A German central bank official said that the only way to effectively regulate bitcoin and other cryptocurrencies is to pursue a global framework with “the greatest possible international cooperation.”

Director of Germany’s Central Bank Calls for Global Cryptocurrency Regulation

Speaking an event in Frankfurt, Deutsche Bundesbank director Joachim Wuermeling said that “effective regulation” is only possible at the international level, according to a Reuters report.

“Effective regulation of virtual currencies would therefore only be achievable through the greatest possible international cooperation, because the regulatory power of nation states is obviously limited,” Wuermeling said.

To date, cryptocurrency regulation has largely been a piecemeal effort at the national level, reflecting the differing stances that governments have taken toward this new technology.

Many nations, such as the US and Japan, have thus far sought regulatory frameworks that protect retail investors without stifling innovation.

Others, though, have adopted hostile stances. China — once the world leader in both cryptocurrency trading and mining — forced the closure of all domestic bitcoin exchanges last September, and the People’s Bank of China (PBoC) is currently working to make the country less hospitable to miners, forcing them to move to other regions.

While naysayers predicted China’s hostile regulatory framework would spell doom for bitcoin, what actually happened served to confirm Wuermeling’s thesis. The void left by the closure of China’s cryptocurrency exchanges was quickly filled by other markets, allowing countries such as South Korea to emerge as a major market in the global crypto-economy.

South Korea’s domestic cryptocurrency trading market has become so heated that the government has recently implemented restrictions in a bid to curb speculative purchases made by retail investors and minors.

However, as in the case of China’s earlier regulations, it is likely that if South Korea’s new rules do make a serious dent in cryptocurrency trading, the decline in volume will lead to a corresponding increase in another nearby market, most likely Japan.

G20 Nations Call for Cryptocurrency Debate

Wuermeling is only the latest financial regulator from a G20 nation to express the need for an international framework for cryptocurrency regulations.

In December, France’s finance minister called for regulators to debate cryptocurrency regulations at this year’s G20 summit, a proposal for which both Italy and Germany expressed support.

Just last week, US Treasury Secretary Steven Mnuchin made similar comments, stating that while US regulators were equipped to combat the use of cryptocurrency in money laundering schemes, other G20 members are not so well-prepared.

TATA Consultancy Services (TCS) said it has bagged a deal worth more than USD 2 billion from the US insurance group Transamerica, marking its largest contract to date. The contract, which entails transforming Transamerica’s US insurance and annuity business lines, comes close on the heels of a mega deal TCS had clinched from television rating measurement firm Nielsen.

“The multi-year agreement (with Transamerica) is worth more than USD 2 billion in revenues, the largest contract signed by TCS to date,”TCS said in a statement. The partnership enables Transamerica to rapidly enhance its digital capabilities, simplify the service of more than 10 million policies into a single integrated modern platform, it added.

The announcement comes a day after TCS reported 3.6 per cent fall its its net profit to Rs 6,531 crore in the December 2017 quarter. “TCS will provide valuable administration and quality customer service, and Transamerica will continue to engage with our customers, clients and advisors in the most meaningful ways to them by utilising our digital engagement platforms and developing new solutions that help people save, protect, invest and retire,”Mark Mullin, Transamerica President and CEO, said. The agreement is expected to lead to annual run-rate savings of about USD 70 million initially –growing to USD 100 million over time –for Transamerica, the statement said.

TCS said it will make job offers to all of the applicable Transamerica employees currently supporting the life insurance, annuity, supplemental health insurance, and workplace voluntary benefits business lines. This, it said, will ensure “a consistently excellent experience for Transamerica customers and protecting approximately 2,200 American jobs”. It added that employees transitioning to TCS will be given the opportunity to remain in the same US cities where they are currently based.

Market Intel

Seven key trends in corporate payments technology – Corporate payments have evolved significantly over the past few years, enabled by modernised technology platforms. Key trends – Payment hubs, ERP integration, Supply chain financing, Local payment services, Blockchain, Open banking APIs, and Regulatory compliance. Read More

Open Banking and PSD2 are set to shake up the finance industry – Open Banking and PSD2 are coming into force over the weekend. Both sets of legislation will change the way the finance industry works across Europe and the UK, and ripples will be felt around the globe. Read More

Blockchain –unblocking payments –With its advantages of carrying out tamperproof, decentralised and transparent transactions in a decentralized manner, blockchain has applications across many industries, but its most popular use remains the one it was originally designed for –payments. Read More

Canadians ready for biometrics– New forms of authentication, such as fingerprint, facial, and voice recognition, can make unlocking accounts and payments much easier and more convenient than traditional passwords or PINs – which are difficult to type onto tiny keyboards, easy to forget, and can be stolen says survey. Read More

Financial technology becomes fashionable – Last September marked the 10-year anniversary of the introduction of contactless technology in the UK. Since then, more than 㿨billion has been spent through contactless cards. Their usage is projected to rise by a further 317% by 2021. Read More

Exchanges call for global fintech standards – As new technologies such as AI and DLT transform the capital markets landscape, the World Federation of Exchanges (WFE) has called on regulators to hold new fintech entrants to the same standards as established players. Read More

Google puts its brand behind payments – Google is merging its disparate payment programmes, including Android Pay and Google Wallet, into a single brand dubbed Google Pay. Google says the initiative is intended to provide consumers with a consistent and simpler way to pay for purchases, whether online or on the high street. Read More

Client/Prospect Intel

CIBC Innovation Banking unit launched to help grow startups – CIBC introduced CIBC Innovation Banking, a full-service business that delivers strategic advice and funding to North American technology and innovation clients at each stage of their business cycle, from start up to IPO and beyond. Read More

Yes Bank to offer ATM withdrawals using Aadhaar ID and biometric authentication – Nearby Technologies has partnered with YES BANK, India’s 5th largest private sector bank and worked closely with National Payments Corporation of India (NPCI) to launch a card less and PIN-less Aadhaar ATM service. Read More

ICICI strikes digital mobility deal with transportation app Ola – The Bank has struck a deal to provide co-branded cards as well as digital loans, ride booking and payments to transportation utility Ola via the bank’s mobile apps.Ccustomers will be able to book cab and pay through the bank’s mobile banking applications, ‘iMobile’and ‘Pockets’. Read More

TD and CIBC wrap up acquisitions as Canadian innovation race intensifies – CIBC signed a deal to snap up Wellington Financial, a firm which provides growth capital to early and mid-stage technology companies. It’s set to become part of CIBC’s Innovation Banking unit, focused on giving advice and funding to clients in the technology sector. Read More

Competition Intel

NLB pioneers Temenos’T24 R17 core banking tech – Slovenian bank NLB has become one of the first live sites of the R17 version of Temenos’T24 core banking system. The bank states it’s keen to attract top talent as part of its digital transformation strategy. NLB moved from R12 to R17 of UniversalSuite which took almost six months to complete. Read More

Conister Bank in core banking tech revamp with TCS – Conister Bank, a community bank in the Isle of Man, is modernising its core banking platform. The bank is replacing its legacy Bankmaster system, supplied by Finastra (formerly Misys). It is understood the new system is TCS Bancs from India-based TCS Financial Solutions. Read More

Janata Bank moves merged and acquired banks to Oracle FFS Flexcube – Nepal’s Janata Bank has moved new data from merged and acquired entities to the Oracle FSS Flexcube core banking system with the help of JMR Infotech. The data from the merged Triveni Bikas Bank and theSiddhartha Development Bank were moved to Flexcube. Read More

Avaloq expands global leadership team – Chris Beukers has been appointed Regional Manager Asia Pacific, Tobias Unger has been appointed Regional Manager Switzerland and Liechtenstein, and Brian Hurdis has been appointed Chief Service Delivery Officer. Read More

TCS bags biggest-ever deal from Transamerica – TCS said it has bagged a deal worth more than USD 2 billion from the US insurance group Transamerica, marking its largest contract to date. The agreement is expected to lead to annual run-rate savings of about USD 70 million initially –growing to USD 100 million over time –for Transamerica. Read More

Eight US credit unions to move to FLEX core banking tech in 2018 –The credit unions that moved to FLEX in 2017 are: Members First, Caprock Federal, Honolulu Federal, Lubrizol Employees’,Wellspring Federal, Coloramo Federal, Kings Peak, Parks Heritage Federal. Read More

Kreditech picks Mambu for expansion into India – Mambu has announced a deal with German company Kreditech, AI-based digital consumer lender, to support the lender’s entry into the Indian market in the first quarter this year 2018. Kreditech already has operations in Europe and Latin America. Read More

Lombard Risk agrees to Vermeg takeover offer – The board of UK-based banking and compliance software firm Lombard Risk has accepted a cash for shares offer from Dutch software firm Vermeg. Lombard Risk’s board has described the deal as “fair and reasonable”, recommending its shareholder to vote in favour of the takeover. Read More

Thomson Reuters goes live with MiFID II – The new services are part of Thomson Reuters commitment to providing a comprehensive suite of solutions to assist the financial services industry with ensuring ongoing compliance with MiFID II requirements. Read More

Along with Bitcoin’s well-documented, meteoric rise from less than $1,000 at the start of the year to more than $16,000 today, the digital currency is making a surprising entrance into the mainstream financial world as well. Last weekend, Cboe Group launched its much-lauded futures contracts, and CME Group will follow them this weekend. These products have attracted a lot of attention, and it’s likely that they are just the beginning of speculative financial offerings related to cryptocurrencies.

Of course, Bitcoin’s founder Satoshi Nakamoto originally intended for Bitcoin to be a decentralised, P2P payment system that is impervious to national borders and is unassociated with large corporations. In short, Nakamoto envisioned a currency that, surprisingly enough, would allow people to buy stuff.

Ebay is harkening Nakamoto’s original intention as it considers accepting Bitcoin as payment on its online auctioning platform. According to various news sources, the conversation has extended to the highest levels of company management. In an interview with Yahoo Finance, eBay’s senior vice-president said they are “seriously considering” accepting Bitcoin as a payment medium.

Ebay boasts a market cap of more than $39 billion, and it enjoys name recognition as one of the most prolific online marketplaces in the world. It reaches more than 100 million shoppers each month, and Bitcoin’s integration into the platform would be a significant step toward mainstream integration of Bitcoin as a payment system.

If it can incorporate Bitcoin, eBay would join a short list of other companies that allow such payments at checkout. Online retailer Overstock and virtual travel agency Expedia are two of the most prominent companies to accept it as payment. Interestingly, for Overstock, this is, in part, an investment strategy. In an August earnings call, Overstock CEO Patrick Byrne acknowledged that the company’s board approved a plan to hold 50% of their received Bitcoin in an investment account.

Because its value is surging so quickly, it allows Overstock to achieve additional earnings from its appreciation. For Overstock, this is an opportunity, but for those wanting to use Bitcoin to buy things, it’s a hindrance.

Nobody wants to purchase a depreciating asset with a currency that’s appreciated more than 1,500% this year. In fact, enthusiasts have an annual celebration for a poor Bitcoin investor who made this mistake.

On 22 May 2010, a now infamous developer, Laszlo Hanyecz, embarked on a mission to test Bitcoin’s usability. The man posted a request for two pizzas on a Bitcoin forum. He agreed to pay 10,000 Bitcoins for the pizzas and delivery. It worked, and his pizzas were delivered a short time later.

Hopefully, the pizzas were really good because those Bitcoins are now worth about $20 million. 22 May, now known as Bitcoin Pizza Day, is an annual recollection of the man’s plight, and it serves as a hilarious and unfortunate reminder that holders should act wisely when spending their digital tokens. It’s difficult to imagine many people risking a similar fate by purchasing a garage sale item on an eBay auction.

In a 2013 interview with The New York Times, Hanyecz did not express any regret for his purchase, noting that he sold the rest of his Bitcoin when it reached the then-impressive price of $1. “That was enough to get a new computer and a couple of new video cards…so I’d say I ended up on top,” Hanyecz told the NYT. As it surges toward $20,000 and some are predicting that it could hit $40,000 by the end of 2018, the reality is that Hanyecz could have attained a lot more.

Still, if mainstream retailers like eBay can successfully integrate Bitcoin and other cryptocurrencies into their payment systems, we might see an entirely digital currency that can serve as an investment asset, a speculative asset, and a usable currency. More developments are still needed, but the conversations are happening, and that’s pretty exciting.

South Korea’s justice minister said that the country is preparing a bill that will ban all cryptocurrency trading

Park Sang-ki told reporters that there are “great concerns” regarding virtual currencies

Bitcoin tumbled more than 12 percent following Park’s remarks

South Korea’s justice minister said on Thursday that a bill is being prepared to ban all cryptocurrency trading in the country.

That news is a major development for the cryptocurrency space, as South Korea is one of the biggest markets for major coins like bitcoinand ethereum.

According to industry website CryptoCompare, more than 10 percent of ethereum is traded against the South Korean won — the second largest concentration in terms of fiat currencies behind the dollar. Meanwhile, 5 percent of all bitcoin are traded against the won.

“There are great concerns regarding virtual currencies and justice ministry is basically preparing a bill to ban cryptocurrency trading through exchanges,” Park Sang-ki said at a press conference, according to the ministry’s press office.

Bitcoin tumbled more than 12 percent following Park’s remarks, according to CoinDesk’s bitcoin price index that tracks prices from four exchanges. At 1:26 p.m. HK/SIN, the cryptocurrency price retraced some of its losses to trade at $13,547.7.

Park added that he couldn’t disclose more specific details about proposed shutdown of cryptocurrency trading exchanges in the country, adding that various government agencies would work together to implement several measures.

Reuters further reported that a press official said the proposed ban on cryptocurrency trading was announced after “enough discussion” with other government agencies including the nation’s finance ministry and financial regulators.

The news wire later added that once a bill is drafted, legislation for an outright ban of virtual coin trading will require a majority vote of the total 297 members of the National Assembly, a process that could take months — or even years.

Cryptocurrency trading in South Korea is very speculative and similar to gambling. Major cryptocurrencies like bitcoin and ethereum are priced significantly higher in the country’s exchanges than elsewhere in the world. For example, bitcoin traded at $17,169.65 per token at local exchange Bithumb, which was a 31 percent premium to the CoinDesk average price.

That difference in price is called a “kimchi premium” by many traders.

In fact, earlier this week, industry data provider CoinMarketCap tweeted that it would exclude some South Korean exchanges in price calculations due to the “extreme divergence in prices from the rest of the world” and for “limited arbitrage opportunity.” The exchanges that were removed from the price calculation included Bithumb, Korbit and Coinone.

Last month, the South Korean Financial Services Commission said it was prohibiting cryptocurrency exchanges from issuing new trading accounts. If an exchange does allow new accounts, the government has the ability to take action to either stop trading or shut the exchange down, the commission said in a statement.

The commission added that, since much of the cryptocurrency trading was being done anonymously, users must use their real names.

The government also indicated it would closely monitor banks and would “swiftly” step in to limit fund flows into cryptocurrencies if necessary.

Bitcoin exposed stocks in South Korea took a major hit after the announcement. Shares of Omnitel, which has a bitcoin remittance business, crashed 30 percent, Vidente shares tumbled 29.96 percent, Digital Optics fell 13.7 percent and KPM Tech was down 5.48 percent.

That news from the justice minister comes after the country’s largest cryptocurrency exchanges were raided by police and tax agencies this week for alleged tax evasion, people familiar with the investigation told Reuters.

2017 was a record year for London and UK fintech investment – The UK is Europe’s leading country for global tech investors, with British tech firms attracting more funding than any other European country last year. London’s tech sector brought in the lion’s share of investment, with the capital’s tech firms raising a record ٠.45 billion. Read More

Banking sector continues to see robust growth in Oman – The banking sector in Oman continued to witness reasonable growth in both credit and deposits. The combined balance sheet of conventional and Islamic banks (other depository corporations), taken together, provides a complete overview of the financial intermediation. Read More

UAE serves as financial hub for the Middle East, says Dubai International Financial centre (DIFC) official – Raja Al Mazrouei, chief executive of the DIFC Fintech hive, says the UAE is taking a lead in the whole region by having the regulation, the funding, and the incubators for fintech. Read More

Largest fintech hub to open in Bahrain – According to consortium’s chairman , the hub would utilise its global network and integrated digital platform to help create an ecosystem where innovators and entrepreneurs can connect and collaborate with corporates, investors, regulators and other stakeholders. Read More

Sri Lanka’s central bank mulls rules for cloud computing, fintech – Sri Lanka’s central bank plans to introduce guidelines for the financial sector covering emerging technologies like cloud computing and ‘fintech’or financial technology, Central Bank Governor Indrajit Coomaraswamy said. Read More

EBL launches Bangladesh’s first AI-based banking chatbot – Eastern Bank Ltd (EBL) has become the first bank in Bangladesh to launch an artificial intelligence (AI) based chatbot. EBL’s Digital Interactive Agent (DIA) will communicate with customers via Facebook Messenger. Read More

Jordan Ahli Bank has become the first bank in Jordan to introduce a chatbot service – Rami Al-Karmi, chief innovation officer at the bank and CEO of Ahli FinTech (and also “Master Jedi”, according to his LinkedIn profile), is inviting users to test the bot and provide feedback. Read More

Client/Prospect Intel

Mashreq Bank Receives Nine Awards From Global Finance in London – Mashreq Bank, the UAE’s leading financial institution was presented with nine awards at the Digital Bank Conference and Awards dinner hosted by Global Finance magazine in London, England. Read More

UK challenger banks: who’s who (and what’s their tech) (Updated) – With so many new entrants trying to muscle into the UK banking sector, there is a comprehensive list of the known challengers to date and the technology they are using. Read More

Wall Street Systems takes European Central Bank (ECB) to court over tech deal with rival Openlink – Wall Street Systems, a long-standing supplier of its Wallstreet Suite treasury management software (TMS) to the ECB, filed a lawsuit in response to the bank’s decision to sign a new deal with another TMS provider, Openlink. Read More

Competition Intel

LuLu Exchange tackles AML with Fiserv tech stack – Fiserv announced that LuLu Exchange, which provides cross-border remittance, currency exchange and other financial services for consumers and businesses, has selected Fiserv to enhance its financial crime prevention capabilities and enable its expansion into new markets. Read More

Sopra Steria Plans to Acquire German Firm BLUECARAT – Sopra Steria plans to acquire 100% of the share capital of BLUECARAT, a German firm providing strategic IT Consulting, Agility, Cyber/IT Security and API Management. This proposed acquisition would strengthen Sopra Steria’s position in the German market. Read More

Natixis Chooses Guidewire Core and Digital Products – Natixis Assurances has selected Guidewire ClaimCenter®as its platform for claims management. The insurer has also chosen the Guidewire Digital application, CustomerEngage Account Management, to boost the digital experience of its customers. Read More

Symitar, Member Driven Technologies Expand Core Processing Partnership – Jack Henry & Associates’ Symitar®division announced the expansion of its partnership with Member Driven Technologies (MDT), a credit union service organization (CUSO). MDT provides credit unions with a private cloud alternative for core processing and IT needs. Read More

Motor City Community Credit Union in core banking tech revamp with Fiserv and Celero – Canada-based Motor City Community Credit Union (MCCCU) has signed to implement the DNA core banking platform from Fiserv. Fiserv’s local partner, Celero, will coordinate the migration to the new system. Read More

State Bank of Pakistan completes major core banking tech upgrade – State Bank of Pakistan (SBP), the country’s central bank and regulator, has completed a major upgrade of its core banking software. The bank moved its currency and banking systems from Temenos’legacy platform Globus G11 to T24 R15. Read More

IT security guy turned entrepreneur. Passionate about seamless integration of technology into everyday life. Love travel and meeting new people. Found Powerdata2go in 2016. Twitter @Antony_PD2G You can create a community post just like Antony here.

Antony is a star contributor for Tech in Asia and publishes exclusive, high-value content that serves the Asian tech community. Read more from star contributors here.

While most people think banks are stable and trusted, they actually operate based on a zero-trust assumption (or simply trust no one). Every employee is constantly under check and control (there have been too many stories of insider hacks, misuse of customer money, and money laundering).

Regulators like MAS or HKMA enforce multi-layer risk control mechanisms, generally known as the three lines of defense. The first line is the process owner or the department manager who executes each transaction and follows bank policies. The second is a centralized or independent risk management department. Risk managers do not execute daily operations but oversee the overall operating environment and set risk parameters, operating procedures, and advise first-line managers on risk mitigation strategies.

The third line is what I was doing—risk assurance. Auditors verify high-risk transactions and give their independent opinion to the board.

All three parties and numerous checks and control build a strong risk management mechanism internal to the bank. There are two other layers external to the bank that ensure critical risk controls are not circumvented: third-party independent auditors (PWC, EY, etc.) and financial regulators.

So, one customer transaction at a bank branch could have five different teams reviewing it (line managers, risk managers, internal auditors, external auditors, and regulators). This explains why there are so many transaction records, signatures, approvals, and a huge paper trail when you simply deposit US$100 in your personal account.

Running a zero-trust organization is costly and inefficient, and internet banking doesn’t solve this crucial and fundamental problem (in some cases, it even amplifies distrust). But blockchain, when taken together with distributed ledger technology (DLT), can. This sets the backdrop for my second post on why blockchain matters.

Trusted system

The problem blockchain is trying to solve is how to run a trusted system with trustless people. (Note: I’m not implying that people are trustless or that we live in a trustless world, but a rotten apple spoils the bunch.)

To be more precise, a trusted system refers to a transactional system that produces results according to a rule book. It’s not always legal (i.e. in compliance with the law), but it has to be resilient and stable/predictable. A trusted system gives a consistent truth that can be verified without relying on another system.

Transactions in a trusted system can’t be repudiated—which depends on record immutability—and are irrevocable. However, immutability in software before DLT was vulnerable because of the human factor (e.g. system administrator misconducts). System administrators had all-access rights and were able to alter system parameters.

But a system can only be as good as the people running them in terms of their trustworthiness, diligence, and capabilities. A few malicious or careless human actors can circumvent all advanced security controls. They are the Achilles heel of a secure system.

Immutability alone does not produce a trusted system; it has to decouple from the operating team. Humans, with souls and feelings, are just too erratic to produce consistent and predictable results.

Blockchain and DLT

Blockchain and DLT together eliminate the vulnerability of human interference, as a system built with both technologies can operate without having to trust system administrators.

DLT solves this administrator problem with a decentralized and consensus approach. A DLT network or infrastructure is still run by people but not by one person or team (like employees receiving paychecks from the same boss). “Distributed” means the software is running on multiple independent operating systems by total strangers without any filtering or selection. Anyone with a computer and a network connection can join and contribute to the DLT—no registration, financial deposit, or ID verification needed.

There is also no hierarchy of users in a DLT system, no super-administrators or privileged accounts that can delete transactions in the system. Each transaction must be endorsed by other users. The system follows self-governance according to the rules defined by the software developers.

But how can hundreds of trustless people achieve self-governance and build a trusted system together?

Game theory

Let us simplify the above question by using a story.

A group of students were on a weekend camping trip. They returned late and missed a midterm exam. The students told the professor that they couldn’t come back on time because they had a flat tire. So, the professor said she would give them an extension if they could give the same answer (without consultation) to one question: Which tire?

In this situation, the students have a common goal to answer the question correctly and share the same benefit. Each of them plays the same role—there are no leaders or people with a privilege to answer twice. If all students cooperate and give the same answer, everyone gets a second chance to take the midterm exam (the reward).

Without a central body and coordination, the students do not need any external enforcement, as it is in their self-interest to work together. In game theory, this is a self-enforcing agreement.

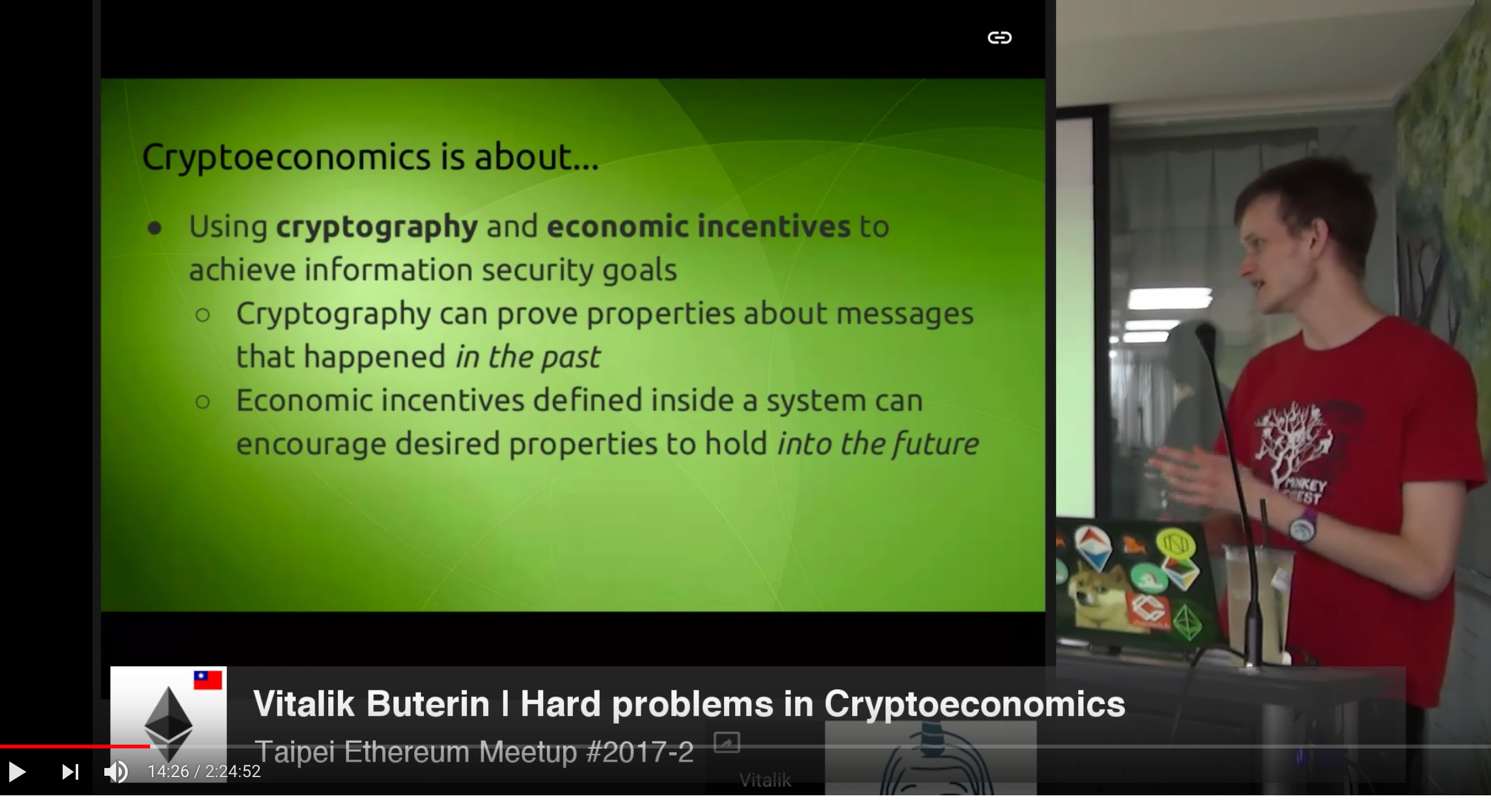

In his talk at the Taipei Ethereum Meetup, Ethereum co-founder Vitalik Buterin said that economic incentives “encourage desired properties to hold into the future.” This means that economic incentives entice each user to behave in a predictable way. Users in a DLT network share the same economic incentive if the DLT is secure and trusted, making each of them act independently and rationally to protect their own benefits.

This economic incentive can exist in many forms: monetary, reputation, etc. In bitcoin, for example, the incentive is generating new coins. Users of the bitcoin DLT are rewarded with a new coin when they fulfill their duty by validating that bitcoin transactions are executed following the bitcoin protocol. The reason new bitcoins are rewarded to users is to encourage them to follow this protocol. (Note: More on this at the bottom of the article.)

Mathematical formulas and cryptography ensure that what happens cannot be altered (immutability), and rewards via the “proof of work” protocol (in bitcoin) ensures the same behavior will be followed by users in the future. Once the system starts, there is no need for central administration.

Drawbacks and risks

Now, we have a system that is traceable and predictable, governed by each user in the system with equal responsibility. Since it is not dependent on human intervention, employing a third party to do independent reviews does not provide additional assurance.

When bank transactions run a blockchain and DLT system, the three lines of defense described at the beginning of this article are no longer necessary. Users trust that the transactions are executed securely, and not because of bank employees, auditors, or even regulators like HKMA or MAS.

But there are also risks in using blockchain and DLT.

Consider the flat tire example again. What happens if there were only two students riding on a motorcycle? There are only four possible permutations and a 50 percent chance that both students will guess the same answer and get another chance to take the exam.

The four possible answers are:

Student A answers front wheel, student B answers front wheel. (Pass)

Student A answers front wheel, student B answers rear wheel. (Fail)

Student A answers rear wheel, student B answers front wheel. (Fail)

Student A answers rear wheel, student B answers rear wheel.(Pass)

It’s not wise for the professor to use the same test. In the case of bitcoin, what happens if only two computers are running the bitcoin protocol? Even though they are independent, it is possible that they make the same error.

One crucial property of DLT is decentralization, which becomes vulnerable if there are only a few independent participants. The risks associated with blockchain and DLT are totally different from the traditional risks of confidentiality, integrity, and availability.

***

Blockchain creates record immutability (past records are safe) and DLT protects immutability from human interference. Game theory enforces the DLT rules by appealing to the self-interest of each individual user (future records are highly likely to be safe).

With these together, we can build a trusted system with decentralized cryptography without relying on third-party auditing. Trust is moved from the auditors to the software infrastructures (one reason why I’m not an auditor anymore).

Did you know that eCommerce is growing 23% year-over-year, and is expected to grow to $4 Trillion by 2020.

This year promises to be another bumper of a year for eCommerce. eCommerce trends set the tone for the year ahead by shaping the direction your business, your design and your marketing will go.

Trends such as Messenger ads and video marketing will continue to dominate and change the way we budget for advertising. While trends such as augmented reality and voice assistant purchases, previously were reserved for big eCommerce brands, could become more accessible to small to medium online business driven by the growing millennial and Gen X shopper online shopper.

The bottom line is: the landscape is changing; changing, but increasing at a phenomenal rate and if you want to up your game this year, getting ahead of these trends will mean more money in the bank. Here are the top 10 eCommerce Trends and Predictions that shape 2018:

eCommerce Trend #1: Messenger Ads to Lead Facebook PPC

Facebook Messenger ads were already hitting some awesome ROI numbers in the last quarter of 2017 and this is expected to climb over the next year. There is a huge push by Facebook to enter the ‘email marketing game’ with their Messenger ads and although this in no way means email marketing is dead (duh!), it is going to have a huge impact on the direct marketing market.

With the rise of Messenger ads we will also see an increase in Chatbots. Chatbots are no longer just for the ‘big guys, with Facebook already offering automatic replies and built in chatbots to small businesses to help simplify the buying process without losing that personal touch.

The new kid (trend) on the block for 2018 is voice shopping. With the surge in popularity of voice-assist products such as Google Home and Amazon Echo, voice shopping is the new best thing in shopping. In fact it is estimated that 40% of millennials are already using their voice assistants to shop online. From the middle of 2017 we saw big retail giants such as Target solidify their partnership with Google voice-assist home products, offering brands a way to streamline customer experience in a whole new way.

For now this technology and marketing trend is out of many smaller eCommerce sites reach, but with the jump to voice-assist shopping on android and iPhone not that far away, the opportunity for smaller to medium eCommerce brands to cash in on the action is in the cards. For now, this is a trend we will watch closely in 2018!

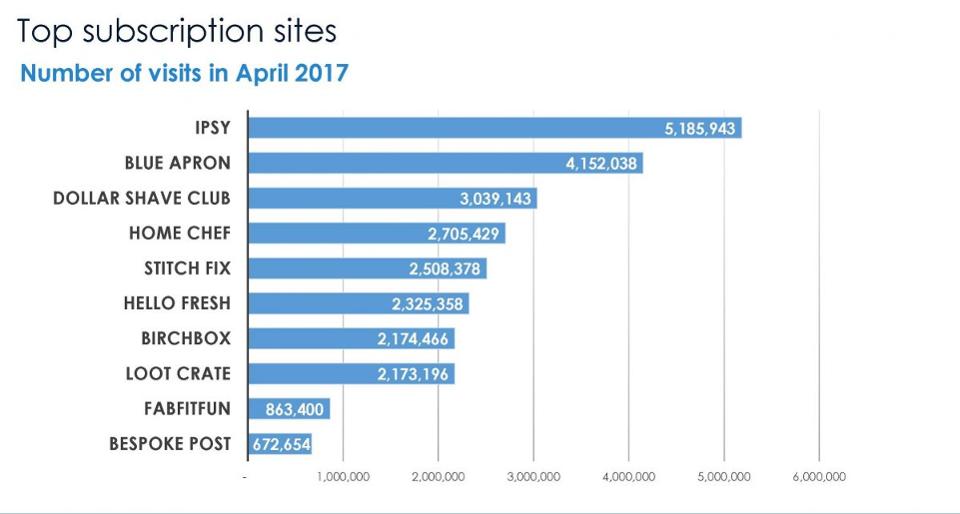

eCommerce Trend #3: Subscription Surges

In 2018 we are expected to see a surge in subscription-based service business models, such as the likes of Forbe’s subscription leaders like Amazon Prime, Loot Crate and Birchbox in smaller online stores. With a definite leaning towards providing more personalized service to create a bigger loyal-customer base in eCommerce, we will see a lot of medium online stores incorporating subscription models into their traditional setups and models.

Still, subscriptions aren’t just about subscription boxes such as tf Loot Crate or providing memberships to fitness programs such as FitGirls, but can be adapted for all sorts of niches. Selling online fashion? Add a seasonal accessory subscription that shoppers can sign up for to get your latest seasonal trends first. Drop-shipping online printed homeware? Why not start a mug-a-month club?

eCommerce Trend #4: More Personalization

I have said it before on this blog: Personalization is so important. However as we go into 2018 it is even more so. This is the year that your marketing needs to be as segmented as possible, where you need to fine-tune your customer service practices like never before and customer experience should be top of your agenda. The bottom line is that customers are getting more and more bombarded by options and in turn online stores will be finding more ways to personalize their shopping experience for customers.

If you can get a jump on that this year, you will be ahead of the pack in time for 2018 final quarter, giving you a big advantage to the big shopping days. Segment your email marketing more so that you are sending products to those shoppers more inclined to buy, optimize your remarketing AdWords campaigns and think small, highly targeted groups, and ensure your site and checkout offers recommended products to customers – all designed to make shopping feel more personal and buying choices easier to make.

Personalization is not just about shopping experience this year. 2018 is set to see an increase in product customization and more fulfillment options as well. Big brands such as Puma are already implementing customized options that help those customers ‘stand out of the crowd’ and buy products they feel are just for them.

Image Source

With the rise of platforms such as Inke, which allow shoppers to buy personalized products in niches from clothes to furniture, we will see the 2017 new-climber move into the eCommerce spotlight and allow smaller online stores to cash in on this action.

eCommerce Trend #6: Augmented Reality for Small Business?

We know AR (Augmented Reality) was a huge buzz word for big retail in the second half of 2017, but will it make mainstream eCommerce in 2018?

Not all of us have an IKEA sized budget to product apps like the above, however, in 2018 we will see more eCommerce and retail superpowers moving towards AR and VR. And with it, the need for online stores to come up with more visual ways – such as virtual dressing rooms – to show off their products in the coming years. We don’t expect this to filter down to small eCommerce just yet, but this is something you should definitely be keeping an eye on in 2018.

If you haven’t invested in a content marketing plan yet, this is your year. Content rich marketing strategies are already being used by most bigger online stores who are said to save $14 on each new customer generated, but in 2018 we will see this filtered down to smaller business who will produce better, more helpful quality content this year.

According to Demand Metric and Hubspot, respectively, interesting content is now one of the main reasons why people follow brands, and marketers who put effort into company blogs are 13 times more likely to generate a positive ROI. This means an increase in things like how-to-videos and Instagram UGC, which will separate those stores who are not seen as helpful authorities in their niche from the rest of the pack and leave them behind.

If you haven’t started using video marketing, 2018 has to be your year. In November we saw ‘amature’ Facebook video views reach as high as 8 million views, bringing in huge fourth quarter revenue.

According to Huffington Post‘s eCommerce predictions for 2018, it is estimated that by 2020, video will make up 80% of all online consumer internet traffic and that video marketing increases your CTR by 200-300%.

What does this mean for you? This year, your content strategy should be all about video marketing and small to medium businesses that haven’t already, need to up their video content game in a big way to keep up with their competitors.

eCommerce Trend #9: More Mobile Shopping

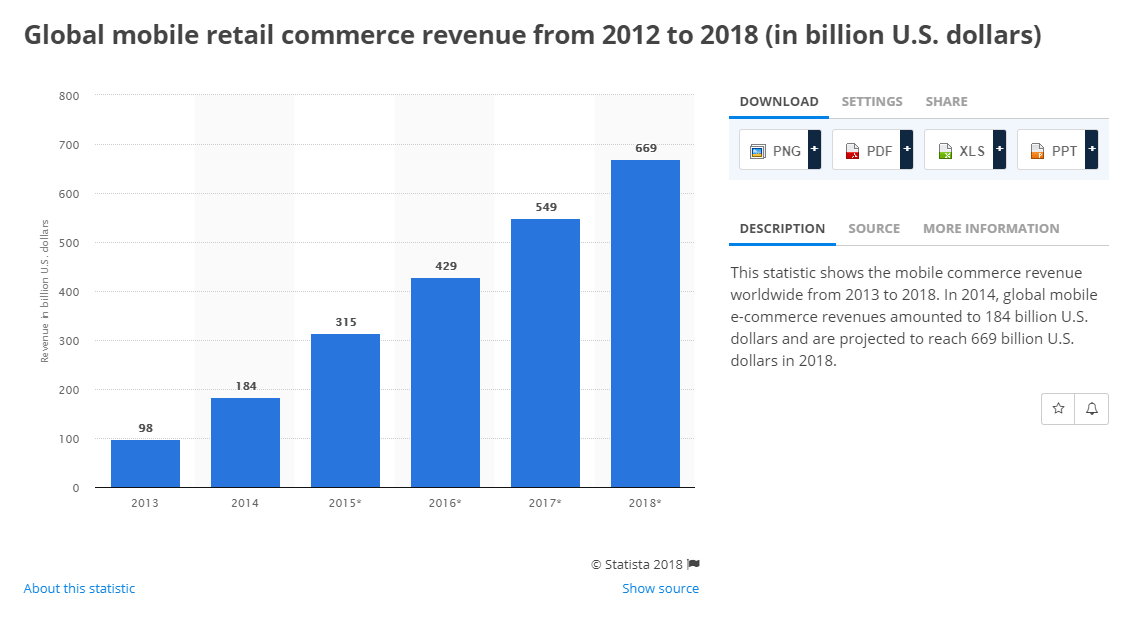

By end of 2018 it is estimated that mobile sales will account for 50% of eCommerce revenue and is set to make up $669 billion worth of sales in 2018, a whopping 20% increase from predictions for 2017. This is the year you want to make sure that you marketing to those mobile shoppers to help you cash in on more sales!

—

There is no doubt about it, with the huge influx of online stores and the global shift from retail to online shopping that continues to climb steadily in the coming year, we’re in for a bumper year. Stay tuned to our blog for up-and-coming 2018 eCommerce trends as we tackle this year with you and guide you through all the tools you need to make this your best sales year ever!

In the world of cryptocurrency trading, learn the following lessons before it is too late :). Good luck mates.

Disclaimer: AbnAsia.org focuses only on the blockchain technology, the technology that Bitcoin and most other cryptocurrency are based on.

1 – Everyone’s a genius in a bull market. Real traders can survive and even thrive in bear markets or highly volatile markets.

2 – Don’t be a blind bull. ALL markets are cyclical. Don’t be afraid of pullbacks or market crashes – that’s where you can make the most money.

3 – There’s a big difference between a trade and an investment.

4 – Fully plan your trade before you pull the trigger on the entry.

5 – Entries are important, but risk & money management is where you make or lose money.

6 – Beware of get-rich-quick gurus hopping on the crypto bandwagon over the past year.

7 – Decide which types of trade setups or investments you’ll take and ignore everything else.

8 – Don’t assume just because you’ve made a lot of money in crypto that you can just as easily make money in other financial markets. 95%+ of stock market traders LOSE money. The game is rigged. Stick to what you know works for you.

9 – The best way to day trade cryptocurrencies is – DON’T!

10 – The best way to profit in any market is to find something you think has big potential early (before the general public catches on), and invest assuming you’re going to lose 100% of your capital. It’s the “angel investor” approach.

11 – You can’t control the market. The only thing you can control is your entries, trade size, and exits.

12 – One market participant can completely destroy “good technical analysis”.

13 – Don’t blindly follow trade alerts from ANYONE, especially random people on social media or chat rooms.

14 – All financial networking marketing projects are ponzi schemes, period.

15 – If you make a life-changing amount of money, do NOTHING for at least 30 days.

16 – Trading isn’t about picking exact tops and bottoms in a market – it’s about catching the meat of a move.

17 – Don’t turn a small losing trade into a massive losing investment.

18 – Don’t set daily profit target goals – set long-term performance goals.

19 – Learn to survive, then thrive.

20 – The best charting indicators are price action and volume. You can use others, but it won’t necessarily make you a more profitable trader.

21 – Trends can go way past what seems rational.

22 – Don’t try to pick tops in a market. Wait for the market to tell you when the trend is over.

23 – Don’t trade in front of big news events – it’s impossible to predict how markets will react.

24 – The biggest challenge for most traders is their ego, or the need to be right.

25 – You can lose 50% of your trades and still be profitable if you manage risk properly.

26 – The best entrepreneurs and CEO’s typically make the worst traders and investors.

27 – People with the best mindset for investing typically have a career in high-risk situations like firefighters, pilots, police.

28 – Avoid pump and dump groups like the plague they are.

29 – You WILL make every mistake in the book. Don’t beat yourself up when you make mistakes, just learn and try not to make the same mistake twice.

30 – Don’t treat crypto exchanges like bank accounts. You don’t own the coins unless you control the private keys.

31 – Crypto is a 24/7/365 market. You can’t catch every trade. If you miss one, don’t worry – there’s ALWAYS another trade.

32 – Don’t invest in a coin unless you understand it inside out.

33 – You can make money trading the momentum and hype in shitcoins, just don’t invest long-term.

34 – Stay away from coins with low trading volume and low market caps. They are easily manipulated and you can get stuck in a position.

35 – Don’t trade with money you need for living expenses. It’s called “risk capital” for a reason.

36 – Think of yourself as a hunter – save your ammo for the big game.

37 – Crypocurrency exchanges go down when there’s high volatility. If price hits a major target or buy zone, it might make sense to place some orders BEFORE everyone else.

38 – Trading and investing brings all your emotions to the forefront – fear, greed, hesitation.

39 – The hardest thing to do in trading is… NOTHING. This can also be the most profitable thing to do.

40 – Just because a market is in a “bubble” doesn’t mean it’s going to die. Bitcoin has been through over half a dozen big bubbles and increased in price after each one.

41 – Manage your trades in a way that would leave you with no regrets no matter what the market does.

42 – Learn to think like a contrarian. If you’re someone who needs to have your opinion validated by everyone around you, then trading and investing isn’t for you.

43 – The shorter the chart time frame, the less reliable the chart patterns are. The longer the time frame, the more variables affect price action and the harder it becomes to predict price. My sweet spot in the daily chart for trade setups and 60-minute chart for entries.

44 – Some market conditions are great for pushing the gas on every trade setup you can find, where other market conditions call for you to slam on the brakes and step away from the markets altogether.

45 – 90%+ of cryptocurrencies will eventually go to zero. Invest accordingly.

46 – The mental side of trading is the hardest to master, the most under-appreciated skill, and will cause you to make or lose the biggest amounts of money.

47 – The 3 biggest problems for traders are over-trading, hesitating on entries, and closing positions prior to profit targets when the trade is still intact.

48 – You can make a career’s worth of profit in one year or one trade – don’t feel like every day has to be a home run. Play the long game. Be patient and wait for the best plays.

49 – Don’t trust anyone else to trade for you. Manage your own high-risk investments (like crypto trading) or don’t participate at all.

50 – Take the news for what it is – they’re trying to get views and clicks. They’re NOT looking out for your best interests or trying to help you make money.

The technology could help Facebook stop being so centralised, he suggested

The technology powering bitcoin could help improve Facebook in the future, Mark Zuckerberg has said.

As part of a commitment to help fix the site over 2018, its founder said that he would look into the use of new technology to stop it being quite so centralised.

One of those technologies is bitcoin, he said, in an ambitious post that suggested Mr Zuckerberg is taking to heart the claims that Facebook is broken

In a long post on his own site, the Facebook founder said that he recognised that the problem with the internet is that it is becoming too centralised, and controlled by a few huge companies that include Facebook itself. That was in contrast to people’s vision that the web could be the perfect way of distributing and decentralising power, he said.

“A lot of us got into technology because we believe it can be a decentralizing force that puts more power in people’s hands. (The first four words of Facebook’s mission have always been “give people the power”.) Back in the 1990s and 2000s, most people believed technology would be a decentralizing force,” he wrote in a long post.